Where is Europe’s Big Tech Sector?

Featuring Original Interviews with European CEOs and Founders

Although Europe is home to 30% of the world’s leading deep tech universities and produces twice as many science and engineering graduates as the US, its technology sector seems modest in comparison. Both the US and China have been able to build international technology champions, with Europe falling behind in competitiveness. For example, the Draghi Report found that no EU company set up from scratch in the previous fifty years has achieved a market capitalisation over €100 billion, whilst the US has produced six that have achieved valuations of over €1 trillion in the same period. The most significant factors restricting growth continue to be heavy European regulation and poor access to capital markets, which has produced a weak culture for scaling businesses. This article will examine all of these factors and will feature interviews from key European founders and CEOs.

The Draghi Report:

In 2024, former Italian Prime Minister Mario Draghi was tasked by the EU to prepare a report on the state of European competitiveness. His report reached three main conclusions. Firstly, Europe must close the innovation gap with the US and China, especially in advanced technologies. EU companies have become specialised in mature technologies where there is less potential for a breakthrough. As such, they spent €270 billion less in 2021 than their US counterparts on research and innovation (R&I). The top EU companies for R&I spending continue to be automotive companies, whilst top US innovators have transitioned towards technology. Secondly, there must be a joint plan for decarbonisation and competitiveness. Europeans pay 2-3 times more for electricity and up to 5 times more for natural gas than Americans. This is partially due to a lack of natural resources, but also due to issues with the common energy market as market rules, high taxes and rents all raise energy costs for end consumers. Over the medium term, decarbonisation will allow for widespread access to low-cost clean energy, but until then energy insecurity and high prices will dampen growth for European companies. The third finding is a need for increased security; rising geopolitical uncertainty can disrupt trade and block investment as Europe becomes increasingly dependent on supply of critical materials and digital technology.

Reliance on American Technologies:

As just mentioned, Europe is especially reliant on America for access to digital technologies. This is especially visible with the cloud as Amazon, Microsoft and Google now account for 70% of the European cloud market between them, whilst European providers only capture 15% of their domestic market. This is down from 29% in 2017. European providers have not stood still – they have more than tripled their revenues from 2017 to 2024, but the market grew by a factor of six, to €61 billion in 2024. This dependence on US technology has spiralled into security concerns, as the American 2018 CLOUD Act gives the US access to data collected in overseas data centres. Karim Khan, the then Chief Prosecutor of the International Criminal Court (ICC), had his Microsoft-hosted ICC email account suspended, following the US sanctions on the ICC. Microsoft denies that it suspended the account, although Khan has now moved to the Swiss Proton Mail as an alternative. The ICC soon followed Khan, confirming in October 2025 that it would replace Microsoft 365 with openDesk, an open-source alternative developed by ZenDiS, a company owned by the German government. Khan has since been suspended from this role; nevertheless, this episode demonstrates how US sanctions are able to weaponise US technologies against European institutions, and how quickly such a threat can translate into European institutions seeking European alternatives.

It is estimated that in 2025, European organisations were spending around €400 billion a year on cloud and software services, €264 billion of which flows into the US economy rather than Europe. This quickly becomes an issue of economic capture, rather than technological dependence. This drain is compounding as the inflation rate for these services is rising several times faster than general inflation. Asterès suggests that by 2030, this could cost the European economy as much as 1.4 million jobs. Payment processors are another huge area of reliance. Visa and Mastercard dominate European card payments: 13 eurozone countries route over 96% of their card transactions through them. For the UK this rises to 98% - a duopoly. This dependence started as a means to improve market efficiency, but has created a situation where European counterparts are struggling to capture their domestic market. Several EU members have created national card schemes that work domestically, but rely on third-party processors internationally. To tackle this, Wero has been launched as a pan-European alternative by the European Payments Initiative, which later partnered with the EuroPA Alliance as a means to connect payments across borders.

As a means to collect revenue on the vast incomes of foreign technological companies in Europe the EU has discussed a broader digital services tax. This already exists in some countries, France has a 3% tax and the UK has a 2% tax, however new discussion of the policy has prompted Trump to threaten a 100% tariff on all goods for any country implementing a digital services tax on US tech companies. The EU responded quickly and firmly, suggesting that it has the sovereign right to regulate economic activities on its territory, and that all taxes are applied equally regardless of the company’s origin. It also stated that it would respond swiftly to protect its rights and regulatory autonomy.

The defining technological race is undoubtedly for AI, and here the capital gap is starkest. The US has already developed a cluster of AI frontier labs; OpenAI and Anthropic are each valued over $850 billion as of mid-2026, whilst Microsoft, Google, Amazon and SpaceX are folding frontier AI into their existing platforms. By comparison, Mistral AI is Europe’s leading challenger, although it is only valued at €11.7 billion as of September 2025 – around one seventieth of either US lab. This huge difference in investment highlights the scale of private capital flowing into US labs, whilst there is no European equivalent. This risks effectively sidelining Europe in the global AI race. Google’s acquisition of DeepMind in 2014 is perhaps the clearest example of an American corporation benefiting from European talent that struggled to scale effectively at home. At the time, DeepMind was celebrated as Europe’s leading AI lab, yet all breakthroughs now accrue to Alphabet shareholders, rather than the British economy. This US dependence is also politically contingent. In June 2026, a US export-control directive barred all foreign nationals from accessing Anthropic’s most powerful Mythos and Fable models – including Anthropic’s own non-US staff. Since Anthropic could not immediately filter for nationality, the result was a complete shutdown of the models in compliance with the US government directive. Access has since been restored, but this example highlights how Washington is able to abruptly switch off access to US technologies overnight, a wake-up call for Europe.

This is not to say that Europe is completely without its own leverage. The Dutch company ASML, spun out of Philips in 1984, is the world’s only supplier of extreme ultraviolet lithography machines which are required to manufacture the world’s most advanced semiconductors. No cutting-edge chips can be produced without this technology. This has been reflected in the company’s market capitalisation of around $700 billion, becoming Europe’s most valuable company ever. ASML has also become an investor in European big tech, leading Mistral’s investment round in 2025. Despite this, the Dutch government still faces significant pressure from Washington to bar ASML’s most advanced sales to China, as part of the US efforts to contain China’s semiconductor industry. One monopoly at one layer of the supply chain does not amount to a complete technology sector, but it does demonstrate that Europe has the potential to capture these huge markets.

Europe’s technological dependence on the US is most visible from orbit. Europe was left unable to launch its own satellites after the Ariane 5 rocket was retired in 2023 and its successor Ariane 6 was delayed by several years. As a result, Musk’s SpaceX was responsible for bringing European Galileo satellites to orbit. Ariane 6 is now operational, but the connectivity gap is even more significant. As of June 2026, Starlink operates over 10,400 satellites, with long term ambitions to expand to 42,000 satellites. By comparison, Europe’s IRIS² 290 satellite programme has only issued its requests for proposals in 2025, initial services by 2030. The security implications of Musk being able to turn Starlink on and off, as he has done in the Russia-Ukraine War, are immense. Even on an accelerated schedule, Europe will spend the rest of the decade paying for its cloud services, payment processors and connectivity from a country that it no longer fully trusts.

Start-ups and Scaling:

Europe does not have an issue with founding companies, but with growing them. Europe is able to generate start-ups at a rate similar to the US, but converts far less into global champions. The bottleneck is undoubtedly access to deep capital markets. 70% of late-stage capital comes from non-European investors, resulting in a quiet ownership transfer out of Europe. Furthermore, Amazon has found that 38% of European start-ups would consider relocating outside Europe to scale, rising to 51% among the highest-growth start-ups. This is in addition to a finding suggesting that almost 30% of unicorns founded 2008-2021 left, mostly for the US. The result of which is that Europe carries the cost of training and initially funding the founders who then often relocate to the US and take their successes with them.

European investors are typically far more risk-averse than US investors. As a result, European institutional investors have long favoured capital preservation over riskier bets that venture capital (VC) often demands. Most significantly, this can be seen with the allocation of pension funds. US pension funds commit over 11 times more VC than their European counterparts. Partly as a result, European start-ups raise roughly half as much private funding over their first decade and struggle to scale in the same way that competing start-ups are able to. In turn, this compounds into slower economic growth and a further reduction of competitiveness.

Two of the European founders who were interviewed for this article have relocated to the US to benefit from greater access to capital markets, a simplified regulatory landscape and a stronger culture of building start-ups. The first is Clément Messeri, the co-founder and CTO of Clema Cooling. Clément suggested that he chose to co-found his company in the US to benefit from strong fundraising opportunities, allowing his firm to raise significant funding pre-revenue. Although Europe does have some grants, policies and other opportunities in place, these do not match the early-stage capital that a start-up needs to launch. On Europe’s position more broadly, Clément said:

“In short, the way I see it. Europe has the talent, the infrastructure, and the policies. The main issue I think is two-fold. They are access to capital, and the networking effect. On the networking front Europe is starting to catch up I’d say. Every major European city has some kind of startup and tech scene. However it is still behind the likes of SF or NYC. Access to capital is the real killer. If it is not a hot topic, like AI is “à la mode” right now, raising significant sums fast, as I understand it, is very difficult in Europe.”

The second European founder who has relocated his start-up to the US is David Khachaturov, founder of Egoist Machines. The company began as a UK venture and has now relocated to San Francisco. The primary driver was greater access to capital markets: in David’s words, the “speed and access to capital is really unparalleled” compared to Europe. Asked whether he would still move his company if Europe offered equal access to capital, David answered: “Probably, as it’s also a cultural phenomenon - from my experience young folk in Europe don’t want to be working 6-9-6 (or more) and unfortunately that’s just what it takes at the moment to succeed.” Regarding what Europe could emulate to develop this culture, David suggested it “needs a mental change of the people to think less about laws and regulations and more about making an impact.” Europe’s lacking start-up culture, similar to that found in Silicon Valley, has been cited by several respondents. Although start-up scenes are developing throughout Europe, they are fragmented across countries, and there is no single go-to destination for tech companies to scale as there is in the US.

Dzmitry Dudzin, the CEO of GanttPRO, a Polish project management software company with over a million users, had the following to say:

“I don’t think Europe has a problem with talent. There are many strong engineers and good products here. The problem is scale.

In the US you have one huge market. In Europe you still have many countries, languages, tax rules, legal details, hiring differences and different customer behaviour. So even inside the EU, scaling often feels more fragmented than it should.

Regulation is also an issue, but I would not say “remove all regulation.” The bigger problem is that it is often too complex and slow for smaller companies. Compliance should be simpler and more unified.

And of course, capital matters. Europe needs more growth funding for companies that already have traction and want to compete globally.

So my answer is simple: make the EU feel more like one real market, simplify rules, improve access to growth capital, and make it easier to hire and operate across countries.”

This highlights the growing issue of compliance costs across borders. An EU company seeking to expand its operations across EU borders faces fresh legal and administrative challenges. This hits smaller companies hardest, but also works to fragment the European market and effectively pressures smaller companies to move to the US rather than grow in the EU. A 2022 report found that small and medium-sized enterprises (SMEs) in the EU face an average cost of 1.9% of turnover for tax compliance. Another 2023 report suggests that 55% of SMEs flagged regulatory obstacles and administrative burdens as their greatest challenge, whilst this was the second most cited challenge for start-ups at 52%, following access to capital.

Ioana Surdu-Bob, co-founder of Konvi, a European alternative-assets investment platform, suggests that they have been able to scale quickly across borders thanks to being able to use the passportable regulatory framework for financial services. This allows Konvi and other financial services companies to expand without the burdensome regulatory and legal costs typically associated with such an expansion.

“For a regulated product, passporting is a huge scaling benefit. I live in Ireland, which is a market of around 5M people. If the licence or framework is passportable across the EEA, the target market grows to 400M+ people. That does not remove national interpretation or local operating costs, but it changes the ceiling completely.”

The EU of course realises that increasing compliance costs have become a considerable barrier for growth. In March, the Commission proposed EU Inc., a new single set of corporate rules to allow businesses to operate and grow across the EU. Harmonising corporate rules means that companies would no longer need to navigate multiple national regulations. The main features include faster business registration (within 48 hours and costing less than €100), full access to the EU single market, fully digital operations and better conditions to attract investment. On EU Inc., Ioana said:

“I think an EU Inc-style structure would be useful, but much less material than passportable licensing. Many cross-border basics already work better in the EEA than people realise: IBANs, instant SEPA payments, cross-border invoicing, and B2B invoicing without charging VAT when both companies are properly EU VAT registered.

There is also more flexibility than people realise. You can incorporate in one country and be tax resident in another. We have used Irish Ltds because Ireland is common law, English-speaking, and everything is online, while having tax residence in civil-law countries such as Germany. Founders will still incorporate wherever it is easiest for their setup, banking, investor expectations, and legal familiarity.”

European Successes:

Despite these financial challenges, Europe has made meaningful progress since the 2024 Draghi Report. The Commission’s 2025 ‘One year on’ review presents the Competitiveness Compass, the EU’s central vehicle to deliver reform on Draghi’s report. The Commission suggests that 90% of its flagship initiatives were drawn from Draghi’s 2024 recommendations, although independent trackers were far more critical, with EPIC’s Draghi Observatory finding that only 43 of 383 recommendations (11.2%) were fully implemented in the first year, rising to 58 in January 2026. Nevertheless, current reforms include the dedicated EU start-up and scale-up strategy, Apply AI strategy, EU Inc., the Clean Industrial Deal and an affordable energy action plan. Additional proposals include the omnibus proposals to reduce regulation, the horizontal single market strategy, the savings and investments union, the union of skills and the competitiveness coordination tool to further encourage European growth.

Most relevant here is the European Technological Sovereignty Package, proposed on 3 June, the clearest signal yet of change in Europe’s digital policy with an emphasis on growing domestic capacity. The Chips Act 2.0 aims to develop domestic advanced semiconductor manufacturing; the Cloud and AI Development Act aims to triple European data-centre capacity and introduce an EU-wide cloud sovereignty framework – reducing the extreme reliance on US firms previously discussed. The Open Source Strategy seeks to scale the long-term move towards open-source software in both public and private sectors. This formalises and expands existing movements away from US software. An example is the German state of Schleswig-Holstein, which has transitioned away from Microsoft software to save approximately €15 million in licensing costs after an initial investment of €9 million. Similar moves have followed in Denmark, France and Italy, although these remain exceptions. Lastly, the Strategic Roadmap for Digitalisation and AI in Energy seeks to use AI to optimise areas most important for the decarbonisation process, such as electric grid optimisation. The explicit objective of these four components is to reduce reliance on non-EU technologies by supporting the domestic industry and ensure that no foreign supplier continues to dominate the key systems that Europe relies on. These legislative proposals are still pending approval in the Parliament and the Council, and the shortcomings of the 2023 Chips Act invite caution. Most importantly, the package relies on private investments that have not yet been committed.

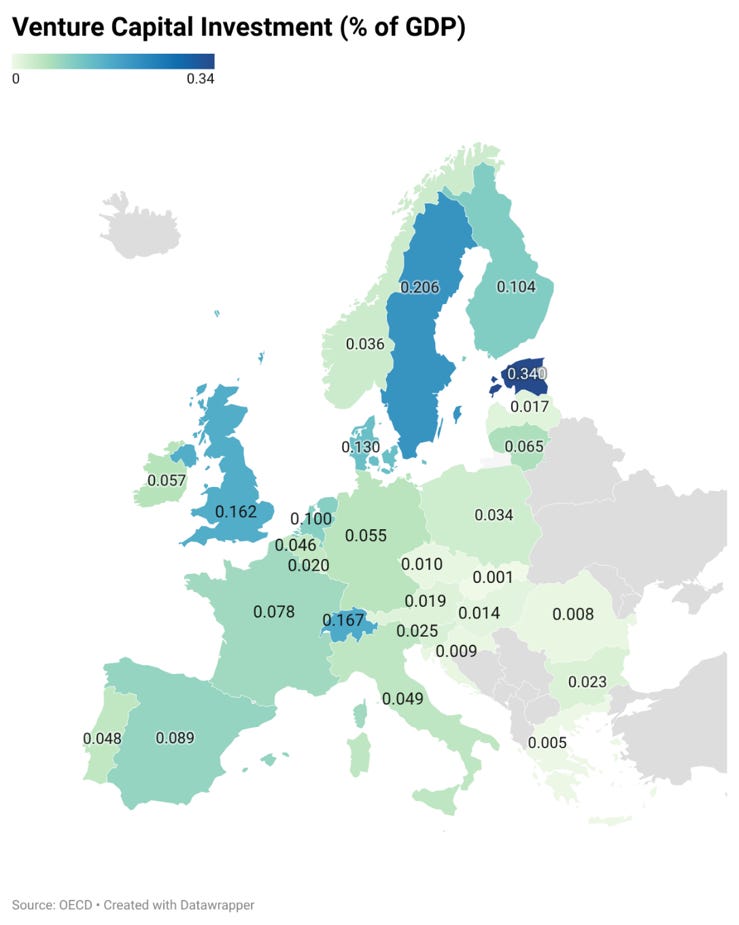

Estonia and Sweden have emerged as the leaders in European start-up and venture capital investments. Estonia has a venture capital investment rate of 0.34% of GDP in 2025, whilst Sweden’s is 0.206%. For reference, the US rate is 0.624%, greatly outperforming even the top European investors. Sweden also tops European R&D Investments in 2024 at 3.57%, compared to the EU average of 2.24%. Estonia trails at 1.99%, but has seen a growth of 0.58 percentage points between 2014 and 2024. As a result, Sweden has developed over 40 unicorns (start-ups now worth over $1 billion), giving Stockholm the highest concentration of unicorns per capita of any city in the world outside of Silicon Valley. They have produced companies such as Spotify, Klarna, Skype, Lovable and more. The success of each is compounding; alumni from these companies often leave to found their own start-ups. The alumni of Klarna, for instance, are responsible for founding 62 start-ups of their own, as founders often become angel investors themselves. This in turn builds a strong support ecosystem, which has been referenced by the founders interviewed earlier, and is fundamental for developing competitive European start-up capitals to rival international competitors. Swedish success is attributed to its higher education, cheap green energy, access to capital markets and a strong social system that encourages risk taking. This must be replicated throughout Europe to further develop the continent into an international competitor.

Estonia on the other hand has developed 10 unicorns, despite having a population of only 1.3 million – the highest concentration per capita of any country in Europe. These companies include Wise, Bolt, Pipedrive and Veriff. Whilst Estonia benefits from a similar alumni-turned-angel-investor flywheel as Sweden, Estonia has also benefited from significant digitalisation. The country has been rebranded as e-Estonia as almost the entire population hold a digital ID, public services run online and a company can be registered in a day. It also boasts an e-residency scheme that allows founders to incorporate an EU company remotely. This combined with a strong education system and a small domestic market pushes founders to think internationally from the beginning. Like Sweden, Estonia offers a strong template for success that the rest of Europe would do well to replicate.

Europe’s predicament is not one of talent or ideas, but of capture. Europe trains some of the world’s best talent but often has to watch it migrate elsewhere as its start-ups scale on US capital, and often relocate to the US. This pattern repeats across each of the layers examined here: European companies rent their cloud storage from US firms, route payments through a US duopoly, watch their leading AI lab raise a fraction of what its US rivals command and then depend on US satellites for connectivity. This was highlighted by the 2024 Draghi Report, which the EU has now sought to address with its ambitious European Technological Sovereignty Package. However, most EU reforms have yet to be fully implemented and very real challenges, such as the limited access to capital markets, remain. Crucially, these dependencies are not structural in a way that a lack of talent or research would be. If the EU manages to implement Draghi’s recommendations in earnest by developing a genuine deep capital market, EU Inc. and supplying abundant cheap energy, then the European economy would benefit greatly from this newfound competitiveness. Estonia and Sweden have demonstrated that member states can become more competitive and grow their own national champions by encouraging education, culture and providing access to capital with lighter regulations; scaled to the rest of the continent this formula would be formidable. The blueprint exists — the only question left is whether Europe can pass serious reforms to improve its competitiveness before another generation of founders move to the US.

If this article was valuable to you, please consider supporting me here or by becoming a paid subscriber. You can also follow this page on Instagram here.