The Incoming Energy Crisis

What the Closure of the Strait of Hormuz Means for Europe and the World

Following the continued US-Israeli offensive against Iran, the Strait of Hormuz has become instrumental for Iran to create international pressure in an attempt to end the war. The Islamic Revolutionary Guard Corps (IRGC) confirmed that the strait was closed on the 2 March, with threats to set ships on fire that violate the order. US-Israeli forces are attempting to gather support to form a naval coalition to forcefully re-open the strait, but allies remain hesitant to directly involve themselves. Iran has attempted to mine the strait in order to complicate the re-opening of the strait, with US-Israeli forces striking the mining ships directly – eliminating 16 by 10 March. Nevertheless, the crisis has created significant supply shocks that will reshape global energy markets in the short-medium term.

The most obvious of these consequences will be the surging price of oil. The price of Brent Crude reached upwards of $100 for the first time since 2022, with peaks nearly 50% more expensive when compared with prices before the war began. An IRGC Spokesperson has claimed that this will go as high as $200 if the war continues. Wholesale gas prices have also reached EUR 52 per megawatt hour, compared to EUR 30 before the war. Whilst the strait of Hormuz controls 20% of the world’s oil supplies, the price increase is not entirely attributed to its closure.

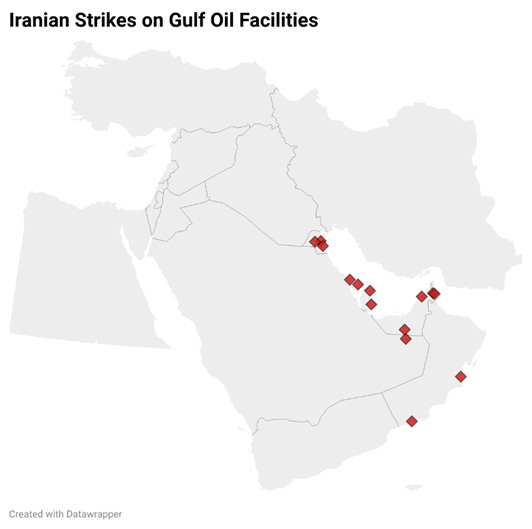

Iran has worked to tactically strike major oil and gas refineries, terminals, storage sites and production facilities, with IRGCN Commander issuing a statement stating that oil facilities associated with America are now on par with American bases and will come under fire with full force. As such, the UAE has reported that a drone has struck the Shah natural gas field and set it on fire. It has been closed as a precaution to assess damage. This gas field is the world’s largest ultra-sour gas operation, with capacity to produce 1.28 bn standard cubic feet of gas a day, as well as 5% of the world’s granulated sulphur. Additionally, a tanker was struck off the major oil port of Fujairah, causing a fire. Operations have been halted here which disrupts the port’s usual export of 1m barrels per day. As a result, the UAE’s daily crude output has halved when compared to export levels before the war. Similar strikes have taken place in Qatar where Iranian drones targeted Qatar Energy (the world’s largest liquified natural gas (LNG) producer) in Ras Laffan, causing them to declare a force majeure on gas contracts on 4 March. This is arguably the single most significant strike on the region’s energy infrastructure as Qatar is one of the world’s top LNG suppliers, and the plant would take a month to reopen. The Ras Tanura oil refinery in Saudi Arabia was also forced to halt operations following a fire caused by a drone strike interception, whilst their Shaybah oilfield has also been targeted. As a result, Saudi Arabia has increasingly been working to divert exports to the Red Sea port of Yanbu, although this pipeline only has a limited capacity and cannot fully accommodate the output previously destined for Hormuz. Multiple strikes have also been recorded in Fujairah, UAE and in Duqm, Oman. This suggests that even routes bypassing the strait of Hormuz cannot be used completely safely. Iraq has gone as far as to try to export oil via Turkey. It is also worth noting that US-Israeli forces have also focused strikes on Iranian oil infrastructure, further compounding the issue of energy insecurity. Kharg Island has stood out here, with Trump ordering significant strikes on Iran’s oil export hub. As a result, total oil/crude flows have dropped from approximately 20 million barrels per day to about 10 million barrels per day.

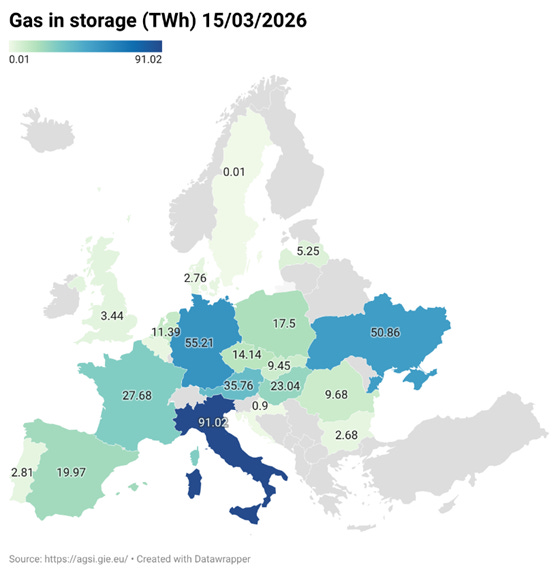

As a countermeasure, the IEA has announced the largest ever oil stock release, with 400 million barrels being earmarked for release from emergency reserves. Future releases may follow if needed. Fuel rationing has begun in countries with low domestic reserves, and a high dependence on Gulf oil, such as Sri Lanka, Bangladesh and Myanmar, with other countries urging austerity measures to reduce consumption. Europe remains more insulated here as only 3.8% of gas imports arrive to Europe from Qatar. The Russia-Ukraine war was a huge wakeup call for the EU’s energy security, and as such significant stockpiles and energy diversification measures have worked to protect the continent in ways that Asia is missing. Nevertheless, increased demand from Asia will still impact the European cost of living, but at an economic level rather than as a question of energy security – at least in the short-medium term. However, Europe’s gas stockpiles going into 2026 were significantly lower than those recorded in previous years, increasing sensitivity to these energy shocks.

It is also worth noting that these strikes have resulted in a huge increase in ship insurance costs for the region. A pre-war insurance cost only around 0.02-0.05% of the ship’s value, whilst it can now cost up to 5%. The US has announced a $20bn reinsurance programme to help revive shipping through the Gulf, as well as temporarily suspending the Jones Act, a shipping law which requires the transport of goods between American ports to be conducted by American-flagged vessels. This is likely another attempt to stabilise the oil price in the short term.

Perhaps the most underreported effect of this crisis is the blockade of fertilisers. The Gulf states produce much of the world’s fertilisers, with approximately one third of the world’s supply transiting the Strait of Hormuz. The most important fertilisers are nitrogen-based products such as urea, which is synthesised from natural gases. This naturally has a compounding effect, as urea production plants across the world will have to reduce outputs following the surging price of natural gas. For example, India produces almost a fifth of the world’s urea/phosphate fertilisers and purchases approximately 40% of its natural gas from the Middle East. Huge price increases in food, as well as very real prospects of food insecurity in the world’s developing countries can be expected, where half of the cost of producing wheat is already spent on fertilisers. Alongside this, the region also exports huge amounts of sulphur which is used to produce phosphates. Morocco will be especially affected here as they control 70% of the world’s phosphate reserves, which must be processed with sulphuric acid in order to become a viable fertiliser. As the Middle East accounts for approximately 44% of the world’s seaborne sulphur trade, it will not be an easy task to find an alternative when countries such as China also have a huge demand.

In order to alleviate these very real global food and energy insecurity concerns, it is vital that the strait of Hormuz be reopened as quickly as possible. However, this is easier said than done. The IRGC has realised that this has become a war for their survival and that by closing the strait of Hormuz they have the power to create international pressure on Trump to seek an end to the war and a return to normalcy. Trump, on the other hand, has weighed forcefully reopening the strait with military presence, involving a potential international coalition and military escorts for tankers and cargo ships. However, international partners are not keen to involve themselves, with spokespeople from NATO countries suggesting politely that this is an American war, not a NATO war. It is also not so clear what Trump hopes to achieve from involving European navies here, the US Navy is already dominant in the region, so this may simply be a means to improve the legitimacy of the war by involving other Western powers. Nevertheless, it remains to be seen if the US will do this independently as they have not yet begun to escort ships as suggested by their Defence Secretary. Notably, the US-Israeli forces have also assassinated Larijani, one of Iran’s de-facto leaders following Khamenei’s incapacitation, on 17 March. Further escalating the war with the IRGC Leadership.

Russia is the natural beneficiary of this Iran war. Surging energy prices massively benefit the Russian economy, much of which will naturally feed into their war effort with Ukraine. The US has also quietly lifted sanctions on Russian oil, at least temporarily, to help with the energy shock. This is a move that is heavily criticised by European leaders, for whom the Ukrainian conflict is much more strategically important. As expected, Ukraine may also suffer from a reduced supply of Western arms following the continuation of the conflict. The EU has remained committed to banning Russian oil/gas, remaining committed to earlier agreements. Hungarian Prime Minister Orban is naturally quick to criticise this, calling for the EU to suspend sanctions. Nevertheless, Von Der Leyen made a statement saying that it would be a strategic blunder to return to Russian oil.

It has also been reported that Italy and France are in negotiations with Iran to allow their ships passage through the strait of Iran. France has acknowledged open communication channels with Iran, whilst Italy has denied direct negotiations. EU Military action has so far has consisted only of individual member states sending ships and aircraft to the Eastern Mediterranean Sea as a defensive move to protect Cyprus. It is possible, but unlikely, that a mission similar to the ASPIDES and ATALANTA operations may be expanded to the Gulf, although nothing official has been confirmed. Kallas, the EU’s foreign policy chief, has indicated that this could be consisted of a “coalition of the willing”. The EU is set to have a leadership summit on 19 March to address the conflict, and a more coherent strategy announcement is expected afterwards. The EU has also activated their crisis management framework across multiple Directorate-Generals in order to coordinate humanitarian assistance, focus on internal and cyber security, as well as to prepare for significant migrant flows into Europe. The UNHCR has estimated that 3.2 million Iranians have become displaced so far, as per their report on 12 March. The Iranian crisis is not just a new cost of living crisis for the EU, but a real test of strategic autonomy, with every policy that the EU has implemented since 2022 to reduce energy dependence being stress tested at once.

This article is not an exhaustive list, nor does it try to be. Information and new updates are constantly coming out as the situation develops. You are encouraged to do your own research.

If this article was valuable to you, please consider supporting me here. Your support will allow me to continue writing without adding any paywalls to stories. You can also follow this page on Instagram here.

The most important line is the last one. Europe has spent three years building energy resilience on the assumption that the next shock would come from Russia. The Hormuz closure is a different kind of shock: it hits the global pricing mechanism, not just the supply chain. Every policy designed for the Russia scenario is now being tested against a threat it was not designed for. That is not a failure of foresight. It is a structural problem: resilience built for one adversary does not automatically transfer to another.

The point about the downstream effects—specifically how a lack of refined oil leads to a shortage of sulphuric acid for metal processing—really highlights the complexity of this crisis. It’s not just about the price at the pump; it’s about the structural damage to industrial output and food security via nitrogen fertilizer production. Given the 200-day recovery estimate you mentioned, do you see this leading to a permanent shift in how nations approach energy sovereignty and maritime security?"